Here’s a REALISTIC take on The economic side of Budget 2015 projections:

Your honest response is invited Minister S Harris, TD?

Gross current expenditure for 2015 will be just over €50 billion. This figure represents an increase of €429 million over the 2014 Revised Estimates.

Note: in H1 2014, Government spent €35.567 billion which is €1.255 billion more than in the same period 2013.

As unemployment fell, social benefits rose from €13.823 billion to €14.016 billion. General Government Deficit has fallen only €307 million year on year in H1 2014.

THESE FUGUES ARE NOT CONSISTENT WITH A STRONG ECONOMY OR A STRONG POSITIVE FISCAL PERFORMANCE.

Meanwhile, the state took out of the economy €1.893 billion more in taxes and social contributions in H1 2014 compared to H1 2013. Where did this increase of funding go?

Government deficit target for 2015 is 2.7% of GDP under ESA 2010 classification. This means that going back to Troika programmes-comparable measure (ESA 1995 classification), the target deficit is closer to 3.2% of GDP. This is ahead of 3% target and shows how much debt we owe not to GOOD MANAGEMENT OF RESOURCES, but to accounting rules changes.

Here’s a set of economic puzzles courtesy of the Department of Finance:

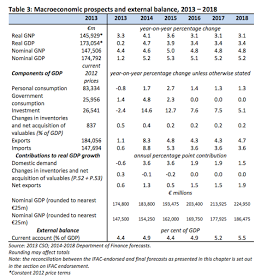

Real growth is slowing down from 2014 levels, but employment generation is rising.

A puzzle?

Especially as domestic demand is expected to grow at same rate in 2015 and growth rate is expected to fall in years after.

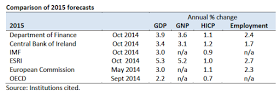

As compared against other organisations forecasts:

Added puzzle:

IMF projections for Irish economy real GDP growth are:-

2015 3.045% – full 0.85 percentage points lower than DofF, 2016: 2.538% which is full 0.87 percentage points below DofF, in 2017 : 2.649% or 0.75 percentage points below DofF… and so on.

And another blatant kick in the teeth… the promise of fiscal rectitude and ‘no going back to boom-and-bust cycles’:

All of the above is rather academic, since the Department of Finance refuses to forecast Gross Voted Current expenditure of the Exchequer beyond 2015, setting all of it at €50.075 billion for each year 2015-2018.

This means the estimated effects on deficit and on borrowing are based on assuming zero growth in spending and continued growth in tax revenues.

Happy times roll on, even though Haddington Road agreement is about to expire.

Still, as you can see, debt/GDP ratio is expected to fall, courtesy of higher GDP, including the new classification effects that came into force this year.

Debt itself is not expected to fall.

Instead, from €203.2 billion, Government debt is expected to rise to &215 billion in 2017 and basically stay there in 2018.

We will be BACK TO SEVERE AUSTERITY AFTER NEXT GENERAL ELECTION, if party politics system prevails in the election.

>>>MARK MY WORDS<<<

On balance: a bit too much optimism, especially past 2015.

Not enough risk cushion.

THE NUMBERS DON'T ADD UP.

You are not being honest and truthful with the sovereign, which is a SACKING offense!